Debt has a way of snowballing quietly. One missed EMI turns into two, the penalty charges start compounding, and before long the outstanding amount looks nothing like the loan you originally took. For a growing number of borrowers in India, that’s the point where “loan settlement” starts coming up as an option usually after restructuring, moratoriums, and repeated calls to the lender haven’t fixed anything.

This piece breaks down what loan settlement actually involves, when it’s genuinely worth considering, and what it costs you in ways that aren’t always obvious upfront.

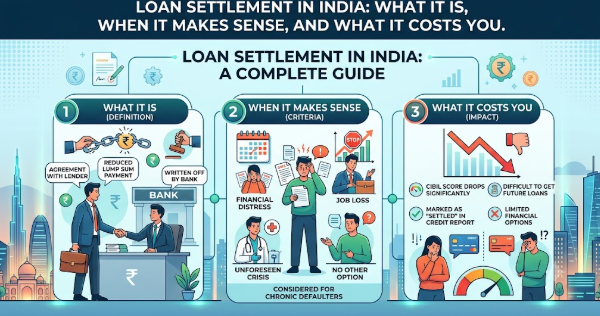

Loan Settlement, Defined Simply

Loan settlement also called a one-time settlement (OTS) or full and final settlement is a formal agreement between a borrower and a lender to close a loan for less than the total amount owed. The lender writes off part of the outstanding balance in exchange for a reduced lump-sum payment, and the account is marked “settled” rather than “closed.”

It applies across personal loans, credit card dues, and NBFC loans, and in India it’s regulated under the RBI’s Framework for Compromise Settlements and Technical Write-offs, which explicitly permits banks and NBFCs to enter into these arrangements with financially stressed borrowers.

Why Lenders Even Agree to This

It seems counterintuitive that a bank would accept less money than it’s owed, but the logic is straightforward. Once an account slips into default, a lender’s realistic alternatives are: pursue costly legal recovery with an uncertain outcome, write off the debt entirely, or negotiate a partial recovery now. For genuinely distressed borrowers, settlement is often the outcome that costs the lender the least in time and legal expense which is why it’s a recognized, legal process rather than some kind of loophole.

When Settlement Actually Makes Sense

Settlement isn’t meant for anyone who simply finds their EMIs inconvenient. It’s built for situations where repayment has become structurally impossible:

1 – A self-employed borrower or small business hit by a prolonged slowdown

2 – Sudden job loss or a significant, lasting pay cut

3 – A medical emergency that wiped out savings earmarked for loan payments

4 – Multiple loans stacking up faster than income can service them

If none of these apply and you can still service your loan with some adjustment, restructuring, refinancing, or debt consolidation are usually better first options settlement should sit lower on the list, not at the top.

The Real Cost: Your Credit Score

This is the part borrowers often underweight. A settled loan doesn’t just disappear from your record it gets marked “Settled” on your CIBIL report, and that status typically stays visible for up to seven years. It’s common for a settlement to knock 75–100 points or more off a credit score, and future lenders will see that “Settled” tag as a signal that you didn’t repay in full.

There’s also a mandatory cooling-off period under RBI’s compromise settlement guidelines generally a minimum of 12 months for non-farm credit during which regulated lenders won’t extend you fresh credit. For wilful default or fraud cases, that restriction can extend further.

None of this means settlement is a bad move for someone in genuine hardship. It just means it should be treated as a deliberate trade-off debt relief now, in exchange for a harder road to fresh credit for the next several years not a free pass.

How the Settlement Process Actually Works

Broadly, the process looks like this regardless of which lender or platform is involved:

Collect your No Dues Certificate (NDC) once the payment clears. This is your proof that the account is fully closed on your end.

Take stock of what you can realistically pay. A lump sum, even a modest one, gives you a stronger negotiating position than showing up with nothing.

Formally contact the lender. This means stating clearly, in writing, why regular repayment is no longer possible.

Negotiate the settlement amount. Lenders in India commonly settle unsecured debt for somewhere between 40–60% of the outstanding amount, and in cases of severe hardship, sometimes as low as 20–30%.

Get everything in writing. A verbal agreement means nothing legally. Insist on a documented settlement offer before paying anything.

Make the payment through traceable channels never cash, never a third party’s personal account.

Can You Recover From a “Settled” Status Later?

Yes this is something many borrowers don’t realize. You can convert a “Settled” status to “Closed” by later paying the remaining waived amount (the gap between the original due and what you actually paid). Once that’s done, the lender issues an updated NDC and the bureau status changes to “Closed,” typically within 30 days. It’s a way to repair your credit history after you’re back on stable financial footing.

Where Third-Party Support Fits

Negotiating directly with a bank is free but puts the entire burden of strategy and paperwork on you, and lenders negotiate settlements professionally every day most individual borrowers don’t. On the other end, informal settlement “agents” often charge 5–15% of the settled amount, and some ask for money upfront with no accountability if nothing actually gets settled a structure that’s attracted a fair amount of fraud in this space.

Dedicated settlement platforms have emerged partly to close that gap offering direct lender access without an agent in between, combined with structured guidance through each step. Zavo, for instance, positions its process around exactly this RBI-guideline-based settlement negotiation, documentation support, and post-settlement credit rebuilding. If you want to see how that specific process is laid out step by step, Zavo has published a full breakdown of the loan settlement process.

Personal Loans vs. Credit Cards vs. NBFC Loans: Does the Process Differ?

The broad mechanics of settlement stay the same across loan types, but a few things shift depending on what you’re settling. Unsecured personal loans and credit card dues fall under RBI’s general compromise settlement guidelines, and lenders tend to have more room to negotiate since there’s no collateral involved. Secured loans home loans, car loans work differently; recovery there is governed by the SARFAESI Act, which gives lenders stronger legal tools, so settlement negotiations on secured debt tend to be tougher and less common. If most of your stress is coming from credit card dues or an unsecured personal loan, you’re generally in a more negotiable position than someone trying to settle a secured loan.

Before You Sign Anything

A few non-negotiables, regardless of which route you take:

1 – Never pay a rupee before you have written settlement terms

2 – Verify any platform or agent is operating within RBI guidelines

3 – Keep every document the settlement letter, payment receipts, and the NDC

4 – Treat settlement as a last resort after restructuring, consolidation, and direct negotiation have genuinely been ruled out

The Bottom Line

Loan settlement is a legitimate, legal way out of a debt situation that’s become unmanageable but it’s not free of consequences, and it’s not the first tool to reach for. Understood correctly, it’s a deliberate trade: a lower payout today in exchange for a temporary hit to your credit standing. For someone facing real financial hardship, that trade can be exactly what’s needed to stop the spiral and start rebuilding.